[ad_1]

Baker Tilly, Mazars USA, and Withum were fined a combined total of $2.14 million earlier this week for breaking various Public Company Accounting Oversight Board auditing rules. Grant Thorntonâs India arm and an Australian audit firm also received penalties from the PCAOB.

The biggest fine was given to top 25 accounting firm Withum, which was docked $2 million on Feb. 21 for âpervasiveâ quality control violations found in its audits of special-purpose acquisition companies (SPACs) in 2020 and 2021.

Those two years saw historic growth in the SPAC market, in which these so-called âblank-check companiesâ (i.e., publicly traded shell companies) raise enough funds through a listing with the intention of acquiring a private company and taking it public. In 2020, there were 248 SPAC initial public offerings in the U.S., up from 59 in 2019. That number shot way up to 613 in 2021, according to Statista.

As the SPAC market grew, Withum and fellow audit firm Marcum served as the main auditors in these engagements. In 2020 and 2021, Withum audited 331 SPAC deals totaling $108.83 billion in value, while Marcum audited 404 SPAC IPOs totaling $108.44 billion in value, Bloomberg Tax reported last September. SPACs generated half of Withumâs $70 million in public company audit fees during the two boom years. Marcumâs SPAC clients contributed a fifth of its $184 million in audit fees, according to Audit Analytics data.

But as the two firmsâ revenues soared, so did their workloads. Missed deadlines and pervasive errors mounted as overloaded partners churned out audit after audit, the Bloomberg Tax analysis found. More than two-thirds of Marcumâs and Withumâs SPAC audits required either a restatement or late filing.

Last June, Marcum was fined $10 million by the Securities and Exchange Commission and $3 million by the PCAOB for several yearsâ worth of quality control failures and violations of auditing standards during its audits of SPACs. The $3 million penalty the PCAOB gave Marcum was the largest doled out to a ânon-affiliate firm,â meaning an audit firm that isnât a member of a global network.

And as part of its settlement with the PCAOB, Marcum was required to create a new role and hire an individual to serve as head of the firmâs quality control system and to create a committee responsible for the oversight function for the audit practice. That was the first time the PCAOB had ever made those demands to an audit firm.

While the sanctions on Withum werenât as severe as Marcumâs, PCAOB Chair Erica Williams said on Wednesday that growth in Withumâs audit practice due to the influx of SPAC clients âmust not come at the expense of quality. The PCAOB will hold firms accountable for upholding quality control systems that protect investors.â

The U.S. audit regulator found that the significant wave of SPAC audit clients from January 2020 through December 2021 put a significant strain on Withumâs quality control system. In 2021, the firmâs issuer audit practice increased almost 500%, from approximately 80 audit reports to almost 450. However, the number of partners assigned to these audits increased by only 50% (from 15 to 23), according to the PCAOB.

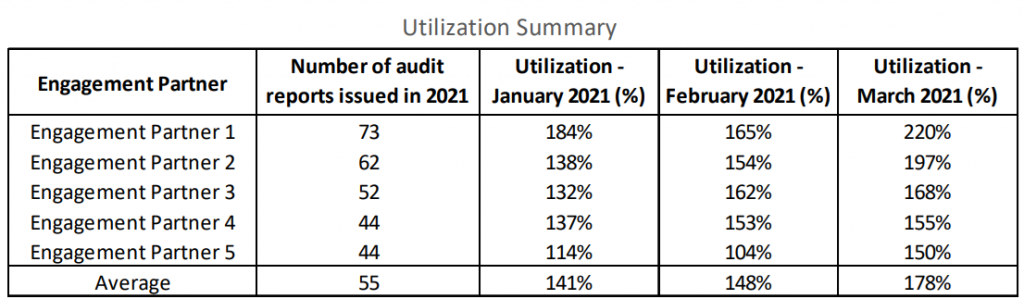

As shown in the chart below, during Withumâs 2021 busy season, from January through March of that year, the average billable utilization for the group of five engagement partners responsible for 40 or more issuer audits was 141%, 148%, and 178%, for each month, respectively, the PCAOB said. In addition to the billable hours worked, these five partners also averaged 15 hours per week on non-billable work over the same period, which further added to the workload for these partners.

Engagement Partner 1, who had the highest number of assigned issuer audits, also had the highest monthly utilization during the period of 220% in March 2021. Moreover, for two weeks during March 2021, Engagement Partner 1 was working approximately 100 hours per week.

Withumâs quality control system failed to provide reasonable assurance that its personnel complied with applicable professional standards and regulatory requirements, including those related to appropriately staffing issuer audits.

The disciplinary order states:

The firmâs system of quality control failed to provide reasonable assurance that the firm would (a) undertake only those issuer engagements that the firm could reasonably expect to be completed with professional competence and appropriately consider the risks associated with providing professional services in the particular circumstances; (b) ensure that partner workloads were manageable to allow sufficient time for engagement partners to discharge their responsibilities with professional competence and due care; (c) ensure that personnel were consulting with individuals within or outside the firm, when appropriate, when dealing with complex issues; (d) perform sufficient procedures to test estimates, including sufficiently evaluating the reasonableness of certain significant assumptions underlying the estimate; (e) make all required communications to issuer audit committees; (f) perform sufficient procedures to determine whether certain matters were critical audit matters (CAMs); (g) perform sufficient procedures to test journal entries; and (h) timely file Form APs.

âTodayâs order should serve as a stark reminder that firms must have both the staff and necessary expertise to perform the audits they agree to perform,â Robert Rice, director of the PCAOBâs Division of Enforcement and Investigations, said on Feb. 21. âIf they do not, we will hold them accountable for those failures.â

Withum settled with the PCAOB, without admitting or denying the findings, and consented to the $2 million civil money penalty. The sanctions also require the firm to engage an independent consultant who will review and make recommendations concerning Withumâs quality control policies and procedures. The firm is also required to conduct certain training for all audit staff.

Baker Tilly and Mazars fined $80,000 and $60,000, respectively

On Feb. 20, the PCAOB said four audit firmsâBaker Tilly, Mazars USA, Grant Thornton Bharat in India, and SW Audit in Australiaâwere found to have violated U.S. auditing rules and standards related to communications that firms are required to make to audit committees. The firms were sanctioned as part of a sweep, which enables the PCAOB to collect information on potential violations from several firms at the same time.

âEngaged and informed audit committees play a key role in promoting audit quality and protecting investors, and they must be kept informed in accordance with our standards,â Williams said on Tuesday. âSweeps are a valuable tool in our enforcement toolbox to ensure there are consequences for putting investors at risk.â

Each firm failed to make certain required communications with audit committees, as required by AS 1301, Communications with Audit Committees.

Three of these firms also violated additional PCAOB rules and standards:

- Baker Tilly failed to document pre-approval of statutory audit services, in violation of AS 1215, Audit Documentation.

- Grant Thornton Bharat failed to ensure that an issuer clientâs audit committee received a copy of managementâs representation letter, in violation of AS 1301 and AS 2805, Management Representations.

- SW Audit failed to satisfy independence requirements in violation of PCAOB Rule 3520, Auditor Independence, and PCAOB Rule 3524, Audit Committee Pre-Approval of Certain Tax Services, by failing to obtain audit committee pre-approval of tax compliance and other services and by engaging an issuer audit client pursuant to an indemnification agreement. SW Audit also violated PCAOB quality control standards in failing to maintain effective policies and procedures with respect to independence and audit documentation.

Without admitting or denying the findings, top 10 U.S. accounting firm Baker Tilly was censured and fined $80,000; top 35 firm Mazars USA and SW Audit were both censured and each fined $60,000; and Grant Thornton Bharat was censured and fined $40,000.

Each firm also consented to comply with revised policies and procedures concerning adherence to PCAOB rules and standards related to these violations.

[ad_2]

Source link